Introduction

Running a small business involves taking many risks—financial, operational, and legal. Unexpected events like property damage, lawsuits, or employee injuries can cause significant setbacks or even threaten the survival of your company. That’s why insurance is a critical element in protecting your business’s future.

Small business insurance plans are specifically designed to cover risks faced by businesses like yours. They provide financial security, peace of mind, and a safety net so you can focus on growth and success. This article explores how insurance small business plans work, the types of coverage available, and how they help safeguard your company’s future in an ever-changing market.

Understanding Small Business Insurance

What Is Small Business Insurance?

Small business insurance refers to a variety of insurance policies tailored to protect small businesses from potential risks and losses. Unlike personal insurance, these plans address the specific needs of business operations, assets, liabilities, and employees.

Why Is Small Business Insurance Important?

No matter the size or industry, every business faces risks. Insurance protects against financial loss resulting from events beyond your control, such as theft, natural disasters, legal claims, or workplace accidents. Without adequate coverage, these events can deplete your capital or force you to close your doors.

Key Types of Insurance Small Business Plans

General Liability Insurance

This is one of the most fundamental types of insurance for small businesses. It protects against third-party claims related to bodily injury, property damage, or personal injury occurring on your premises or because of your business operations.

Property Insurance

Covers damage to your physical assets such as buildings, equipment, inventory, and furniture caused by fire, theft, vandalism, or natural disasters. For businesses operating from home, it often complements homeowners’ insurance.

Workers’ Compensation Insurance

If you have employees, workers’ compensation insurance is typically required by law. It covers medical expenses and lost wages if employees get injured or fall ill due to work-related incidents.

Professional Liability Insurance

Also known as errors and omissions (E&O) insurance, this plan protects against claims of negligence, mistakes, or failure to perform professional duties that result in financial loss for a client.

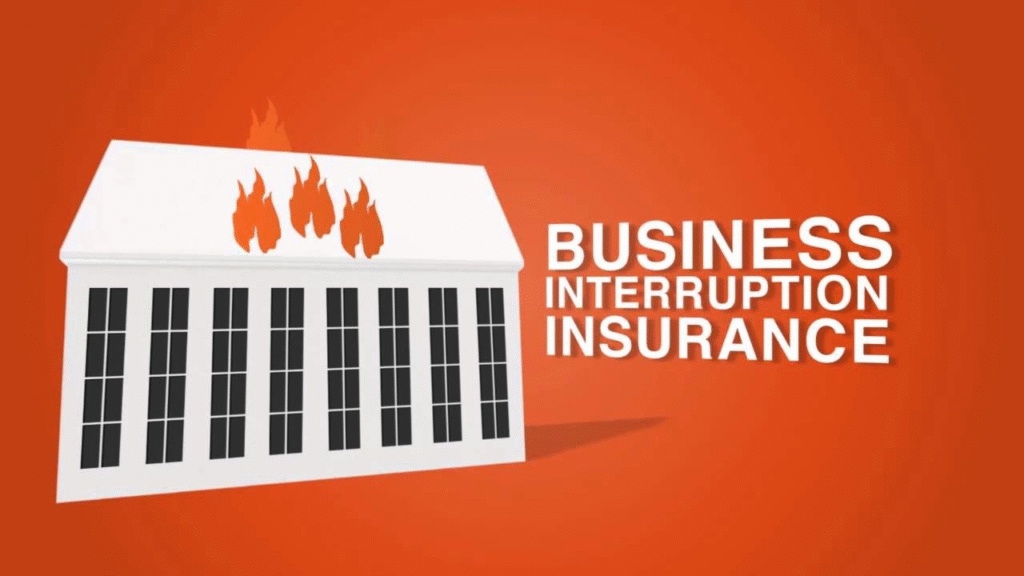

Business Interruption Insurance

If your business operations are halted due to a covered event such as a fire or flood, this insurance helps replace lost income and covers ongoing expenses during the downtime.

Commercial Auto Insurance

For businesses that use vehicles for operations, this insurance covers damages or injuries caused by business-owned vehicles.

Cyber Liability Insurance

As digital threats increase, cyber liability insurance protects your business from losses caused by data breaches, hacking, and other cyberattacks.

How Insurance Small Business Plans Safeguard Your Future

Financial Protection Against Unexpected Losses

Insurance policies help cover repair costs, legal fees, medical bills, and compensation claims. Without insurance, these expenses can drain your resources and cripple your business.

Enhancing Business Credibility and Trust

Having proper insurance coverage reassures clients, partners, and investors that your business is professional, responsible, and prepared to handle risks.

Compliance with Legal Requirements

Many types of business insurance are mandatory, such as workers’ compensation or commercial auto insurance. Meeting these legal requirements protects you from fines, penalties, or business closure.

Securing Loans and Contracts

Lenders and clients often require proof of insurance before approving loans or signing contracts. Insurance demonstrates your business is financially stable and trustworthy.

Protecting Personal Assets

For sole proprietors and small partnerships, business liabilities can put personal assets at risk. Insurance separates business risks and shields your personal property from claims.

Assessing Your Business Insurance Needs

Identify Your Risks

Evaluate the nature of your business, industry, location, number of employees, and operations to determine which risks you face.

Consider Your Business Size and Growth Plans

As your business grows, your insurance needs evolve. Review your policies annually and adjust coverage limits accordingly.

Consult With Insurance Professionals

Working with insurance agents or brokers specializing in small businesses helps you find the best policies tailored to your unique needs.

Understand Policy Details

Review coverage limits, exclusions, deductibles, and premiums carefully. Know what is covered and what is not to avoid surprises during claims.

Common Misconceptions About Small Business Insurance

“I Don’t Need Insurance Because I’m Small”

Even small businesses face risks. One lawsuit or disaster can wipe out years of hard work.

“Homeowners’ Insurance Covers My Business”

Personal policies usually exclude business-related claims or have limited coverage for business property.

“Insurance Is Too Expensive”

While insurance is an investment, the cost of not having it can be much higher. Many affordable options exist based on your business profile.

“I Can Just Handle Legal Issues on My Own”

Legal claims can be complex and costly. Professional liability insurance provides critical protection and peace of mind.

Tips for Choosing the Right Small Business Insurance Plan

Bundle Policies for Savings

Many insurers offer package deals, such as a Business Owner’s Policy (BOP), which combines general liability and property insurance at a discounted rate.

Shop Around and Compare Quotes

Get multiple quotes to find competitive pricing and better coverage options.

Check the Insurer’s Reputation

Research insurers’ financial stability and claim handling records before committing.

Review Coverage Annually

Your business evolves, and so should your insurance. Update your policies regularly to reflect changes in your operations.

The Claims Process: What to Expect

Reporting the Incident

Notify your insurer as soon as possible with detailed information about the incident.

Documentation and Evidence

Provide photos, receipts, contracts, or any supporting documents to validate your claim.

Investigation and Assessment

The insurer will investigate the claim and assess damages or liabilities.

Claim Resolution

You will receive compensation according to your policy terms. Keep clear communication with your insurer throughout the process.

Also Read : The Essentials Of Financial Protection: Insurance, Savings, And Smart Planning

Conclusion

Insurance small business plans are more than just a safety net—they are a vital component of a successful, sustainable business strategy. By protecting your assets, managing risks, and ensuring compliance with laws, these insurance policies empower you to focus on growth with confidence.

While the costs of insurance might feel like a burden at times, the financial security and peace of mind they provide are invaluable. A well-chosen insurance plan can prevent catastrophic losses, help you recover quickly from setbacks, and keep your business thriving for years to come.

Taking time to assess your risks, understand your options, and work with trusted insurance professionals will ensure that your small business is well-protected against the uncertainties of the future.

Frequently Asked Questions (FAQs)

What types of insurance are mandatory for small businesses?

This depends on your location and industry, but typically workers’ compensation and commercial auto insurance (if you use vehicles for business) are required. Some states also require professional liability insurance for certain professions.

How much insurance coverage do I need for my small business?

Coverage needs vary based on your business size, assets, risks, and legal requirements. A professional insurance agent can help tailor the right limits for your situation.

Can I customize my insurance plan?

Yes. Most insurers offer customizable policies or packages to fit the unique risks and needs of your business.

What is a Business Owner’s Policy (BOP)?

A BOP bundles general liability insurance and property insurance into one package, often at a lower cost than purchasing them separately.

How do insurance premiums get calculated?

Premiums depend on factors like your industry, business size, location, claims history, coverage limits, and deductibles.

Will insurance cover damages caused by natural disasters?

Property insurance often covers certain natural disasters like fire and wind damage. However, some events (like floods or earthquakes) may require separate specialized policies.

Can insurance help with cyberattacks?

Yes. Cyber liability insurance protects against data breaches, ransomware attacks, and other cyber risks.

What happens if I don’t have insurance and face a lawsuit?

You may have to pay damages out of pocket, which can be financially devastating and could lead to bankruptcy or business closure.

How often should I review my insurance coverage?

Review your policies annually or whenever you experience significant business changes, such as expansion, new products, or additional employees.

Is it worth bundling multiple insurance policies?

Bundling often reduces costs and simplifies management. However, always compare bundled offers against individual policies to ensure you get the best coverage.